You won your civil case. The court entered a judgment in your favor. Then nothing happened. The debtor has not paid, has not called, and may not even be reachable at the address you have on file. You know you are owed money. You do not know where that money is.

This is one of the most common situations judgment creditors face in California, and it is exactly the problem a judgment debtor examination is designed to solve. It is not a new lawsuit. It is not a negotiation. It is a court-ordered hearing where the debtor must appear before a judge, answer questions under oath about their finances, and tell you where their money is.

This article covers how the process works under California law, how to schedule one, what to ask, what documents to request, and what to do with the information you collect.

What Is a Judgment Debtor Examination

A judgment debtor examination, sometimes called an order of examination or a debtor exam, is a post-judgment discovery tool available to California judgment creditors under California Code of Civil Procedure section 708.110. After a court judgment has been entered and remains unpaid, the creditor can compel the debtor to appear in court and answer detailed questions about their financial situation.

The debtor is placed under oath. Everything they say is subject to perjury laws. They are required to disclose bank accounts, employment, real property, vehicles, business interests, pending legal claims, and any other assets or income sources the creditor asks about. The court does not examine you. You or your attorney ask the questions directly, and the debtor must answer truthfully or face legal consequences.

This procedure is available for civil money judgments from California Superior Courts, federal district courts sitting in California, and small claims courts. It applies whether the judgment debtor is an individual or a business entity.

When to Use a Debtor Examination

The debtor exam is most useful in three situations.

The first is when you do not know what assets the debtor has. Before you can garnish wages, levy a bank account, or record a property lien, you need to know where those assets actually are. A debtor exam puts the debtor under oath and requires them to tell you. One hearing can give you the employer name, the bank name and branch, vehicle information, and property addresses you need to take action.

The second is when earlier enforcement attempts failed. If a bank levy came back empty or a wage garnishment lapsed because the debtor changed jobs, a debtor exam lets you update your information and pivot to a new approach. Debtors who have moved money, changed employment, or transferred property since the judgment was entered can be required to account for those changes.

The third is when you suspect the debtor is hiding assets. Debtors sometimes transfer property to family members, open accounts in other people’s names, or structure their finances to appear judgment-proof. The debtor exam puts them under oath and creates a formal record of their financial claims. If the testimony later turns out to be false, contempt of court and perjury charges become available tools.

How to Schedule a Judgment Debtor Examination in California

The process begins with the court that issued the judgment, or in the case of a small claims judgment, the small claims division of that court.

Step 1 — File the application. File an Application and Order for Appearance and Examination using Form EJ-125 (for civil judgments) or Form SC-134 (for small claims judgments) with the court clerk. Pay the filing fee, which varies by county but is typically between $20 and $40. The clerk will issue the signed Order for Appearance, which sets the hearing date and commands the debtor to appear.

Step 2 — Serve the debtor personally. Under CCP 708.110(b), the Order for Appearance must be personally served on the debtor at least 10 days before the hearing date. Personal service means a licensed process server or the county Sheriff must physically hand the order to the debtor — mailing it or leaving it with a third party does not satisfy this requirement.

This is often where creditors run into difficulty. A debtor who suspects an examination is coming may avoid their home, not answer the door, or have moved to a different address. If service cannot be completed before the scheduled hearing date, the hearing will need to be rescheduled and re-served. Using a professional process server who knows how to locate and serve evasive individuals saves significant time at this stage. If the debtor’s address is unknown entirely, skip tracing services can locate a current address before the application is even filed.

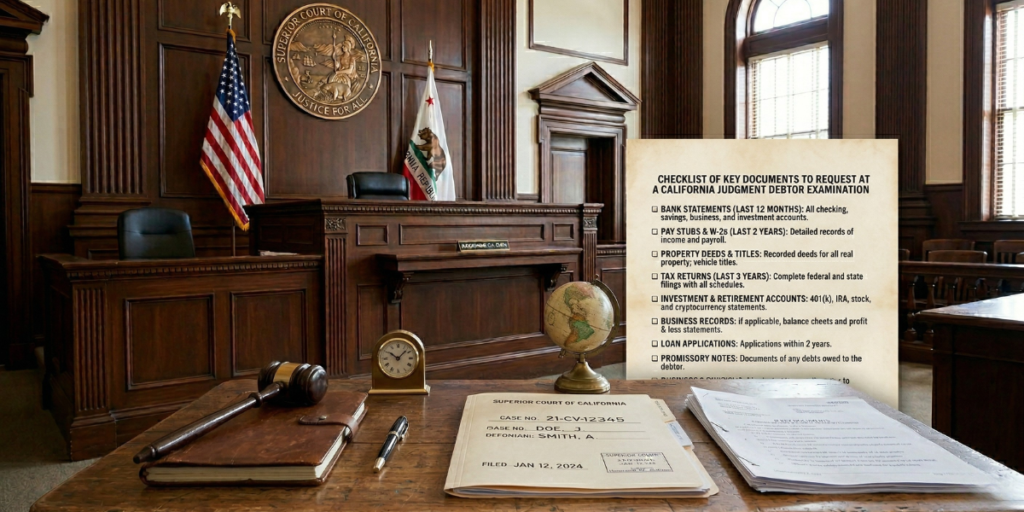

Step 3 — Request a Subpoena Duces Tecum. Before the hearing, request a Subpoena Duces Tecum from the court ordering the debtor to bring specific financial documents to the examination. This is a separate form from the Order for Appearance and must also be personally served on the debtor. Request documents, including recent bank statements, pay stubs, tax returns, vehicle titles, property deeds, and records of any pending legal claims or settlements the debtor is a party to. Documents in hand at the hearing let you verify answers and catch inconsistencies immediately.

Step 4 — Appear at the hearing. Both you and the debtor must appear at the scheduled time. The hearing takes place before a judge or court commissioner. You conduct the questioning. No opposing attorney is examining you. The hearing is generally not a formal deposition, but the answers are given under oath, and the court may intervene if questions or objections arise.

What to Ask at the Hearing

The scope of permissible questions at a judgment debtor examination is wide. Under CCP 708.130, the debtor may be examined regarding their property, their income, and any property they may have transferred to others. The following categories cover the most valuable areas.

Banking and financial accounts: Ask for the name, address, and account numbers of every bank, credit union, brokerage account, or payment processor account the debtor holds or has held in the past two years. Ask specifically about payment platforms such as PayPal, Venmo, Stripe, and Square, which many small business owners and self-employed individuals use as their primary banking channel. Ask whether any accounts are held jointly with a spouse or business partner.

Employment and income: Ask for the name and address of every employer in the past two years, the pay schedule, and the amount of each paycheck. If the debtor is self-employed, ask for the business name, address, a list of current clients, and how payments are received. Ask about any freelance income, rental income, commissions, or other recurring payments.

Real property: Ask whether the debtor owns or has an interest in any real estate in California or in any other state. Ask for the property address, the assessed value, the outstanding mortgage balance, and the lender’s name. Ask whether any property has been transferred, gifted, or sold in the past two years, and to whom.

Vehicles: Ask for the make, model, year, and license plate of every vehicle the debtor owns or has a financial interest in. Ask whether any vehicles are registered in a family member’s name. Ask about boats, trailers, or recreational vehicles as well.

Business interests: If the debtor owns or has an ownership stake in a business, ask for the business name, address, tax identification number, nature of the business, and the debtor’s percentage interest. Ask whether the business holds any bank accounts, owns equipment, or has accounts receivable.

Pending legal claims: Ask whether the debtor is a plaintiff in any active lawsuit, expects to receive a settlement, or has any pending workers’ compensation or insurance claims. A judgment lien or assignment order can attach to the proceeds of a legal claim before the money reaches the debtor.

Recent transfers: Ask whether the debtor has given, sold, or transferred any property worth more than a modest amount in the past two years, and to whom. Fraudulent transfers made to shelter assets from creditors can be challenged in court, but you need to know they occurred first.

What Happens If the Debtor Does Not Show

If the debtor was properly served and fails to appear at the scheduled hearing, the judge can issue a bench warrant for their arrest. The debtor can then be brought before the court by law enforcement. In practice, the threat of a bench warrant is often enough to bring a non-appearing debtor to a rescheduled hearing.

A debtor who appears but refuses to answer questions, provides obviously false answers, or testifies inconsistently with documented evidence can be held in contempt of court. Contempt sanctions can include fines and, in serious cases, jail time.

Using the Information to Enforce the Judgment

The debtor examination itself does not collect any money. What it does is tell you where the money is so you can use the right enforcement tool to reach it.

If the debtor disclosed a bank account, your next step is a bank account levy using a writ of execution served on that financial institution. If they disclosed an employer, you proceed with wage garnishment. If they own real property, you record an abstract of judgment with the county recorder in that county. If a third party owes them money, you pursue an assignment order or third-party levy.

Some creditors request a turnover order at the conclusion of the examination itself. If the debtor disclosed cash, negotiable instruments, or specific personal property in the hearing room, the judge can order the debtor to hand it over immediately. This is relatively uncommon but worth requesting when circumstances allow.

For creditors managing complex cases involving multiple enforcement methods across different California counties or dealing with debtors who have moved to other states, Ranworks judgment enforcement services coordinate the full post-examination enforcement process on a contingency basis. No recovery means no fee.

Examination of Third Parties

The debtor examination process is not limited to the debtor themselves. Under CCP 708.120, a creditor can also subpoena third parties who know the debtor’s property. This includes banks, employers, accountants, business partners, and family members who may hold assets on the debtor’s behalf.

A third-party examination works the same way as a debtor examination. The third party is personally served, required to appear, and examined under oath. Banks are commonly subpoenaed to confirm account balances and transaction history. Employers are occasionally examined to verify pay rates and deduction schedules. Business partners may be examined if there is reason to believe that company assets are being used to shield the debtor’s personal liability.

This tool is underused by most creditors. The mere scheduling of a third-party examination often prompts debtors to come forward and negotiate a settlement to avoid the disruption and embarrassment of having their associates pulled into court.

How Often Can You Schedule a Debtor Examination

Under CCP 708.110(d), a creditor cannot conduct a new examination of the same judgment debtor within 120 days of a previous examination, unless the court grants permission for an earlier hearing based on changed circumstances. This rule applies to examinations of the debtor as an individual. Third-party examinations have no such restriction.

If a debtor’s financial circumstances change significantly within the 120-day window, such as taking a new job, receiving an inheritance, or acquiring property, you can apply to the court for permission to hold an earlier examination.

Conclusion

A judgment debtor examination is one of the most direct tools California law gives creditors to close the gap between a court order and actual payment. It puts the debtor under oath, requires them to account for their finances, and gives you the specific information needed to use every other enforcement tool correctly.

The procedure is not complicated, but the details matter. Personal service must be completed on time. The right documents must be subpoenaed in advance. The right questions must be asked at the hearing. And the information collected must be acted on quickly before the debtor’s circumstances change again.

If the debtor’s location is unknown, if earlier enforcement attempts have stalled, or if you need professional support coordinating the full enforcement process after the examination, contact Ranworks Legal Support Services at 888-636-0293 or email info@ranworks.com for a case review.

Frequently Asked Questions

Q1. What is the difference between a judgment debtor examination and a deposition?

A deposition is a discovery tool used before trial to gather evidence while the lawsuit is still active. A judgment debtor examination is a post-judgment procedure conducted after the court has already entered a verdict. The two serve different purposes at different stages of litigation. A deposition is governed by the Civil Discovery Act. A debtor examination is governed by the Enforcement of Judgments Law under CCP 708.110. Both require the person being examined to answer under oath, but the procedural rules, filing requirements, and available follow-up actions differ significantly.

Q2. What happens if the debtor lies during the examination?

Testimony at a judgment debtor examination is given under oath, which means false answers constitute perjury under California law. If a debtor’s testimony is later contradicted by documents, bank records, or other evidence, a perjury complaint can be filed. In addition, a debtor who provides false testimony to conceal assets can face contempt of court sanctions imposed by the judge who conducted the examination. Creditors who suspect false testimony should preserve the transcript of the hearing and cross-reference it against any financial records obtained through the Subpoena Duces Tecum or subsequent levies.

Q3. Can a debtor refuse to answer questions at the examination?

A debtor can assert the Fifth Amendment privilege against self-incrimination for questions where an honest answer might expose them to criminal liability. Outside of that limited circumstance, they are required to answer all questions about their finances and assets. A debtor who refuses to answer without a valid legal basis can be held in contempt of court. Objections to the relevance of a question are generally not sustained at a debtor examination — the scope of permissible inquiry under CCP 708.130 is deliberately broad to give creditors access to all information needed for enforcement.

Q4. How long does a judgment debtor examination typically take?

A straightforward examination of an individual debtor with a relatively simple financial situation usually takes between 30 and 60 minutes. More complex cases involving business ownership, multiple assets, suspected transfers, or a debtor who is being evasive can run longer. There is no fixed time limit under California law, though judges may manage the hearing if it becomes repetitive or strays outside the permissible scope. Preparing a written list of questions in advance, organized by category, makes the hearing more focused and reduces the time needed to cover all relevant ground.

Q5. Do I need an attorney to conduct a judgment debtor examination?

An attorney is not required. Judgment creditors representing themselves can file the application, arrange service, and conduct the examination directly. That said, an experienced attorney or professional enforcement service is better positioned to ask follow-up questions on the spot, recognize when an answer may indicate hidden assets, and immediately request a turnover order if the hearing reveals collectible property. For creditors managing larger judgments or dealing with a debtor who is clearly attempting to conceal assets, professional representation at the hearing is worth considering.